Young people are going about investing all wrong. The most basic (and important) decision you make as an investor is your allocation between major asset classes—primarily stocks, bonds, and cash. Here is how millennials’ portfolios look in 2014, according to a recent research report from UBS.

This allocation screams caution, worry, and distrust of the stock market. Why are millennials investing this way? Mainly because they have had two very sour experiences with the stock market: the technology crash between 2000-2002 and the more dramatic financial crisis between 2007-2009. Both times, the market collapsed 40% or more. The only other time that happened twice in one decade was in the 1930’s in the midst of the Great Depression. Millennials don’t trust Wall Street (all four major banks among most hated brands by millennials), and one of our most famous authors is saying the stock market is rigged.

With all this in mind, it makes sense that millennials are so cautious. But the choices they are making with their investments are backwards. Millennials think cash is safe, but its actually dangerous. They think that stocks are risky, but in fact stocks are the safest means to secure long-term financial prosperity.

The problem is that we tend to think of “risk” as a fixed concept—that is, stocks are riskier than cash and bonds…period. But risk can only be accurately assessed in combination with a time horizon. If you are 25 and saving for retirement, you have at least a 40 year time horizon, which drastically changes what is risky and what is safe. Millennials are making decisions as if they were 60 years old, on the verge of retirement—and it could cost them huge amounts of wealth.

The Potential of Every $1

I find it easiest to think about potential investments in terms of individual dollars. What returns are you likely to earn over certain time periods on every dollar you invest? What are the best and worst case scenarios? Let’s start with stocks—the most hated investment choice among millennials.

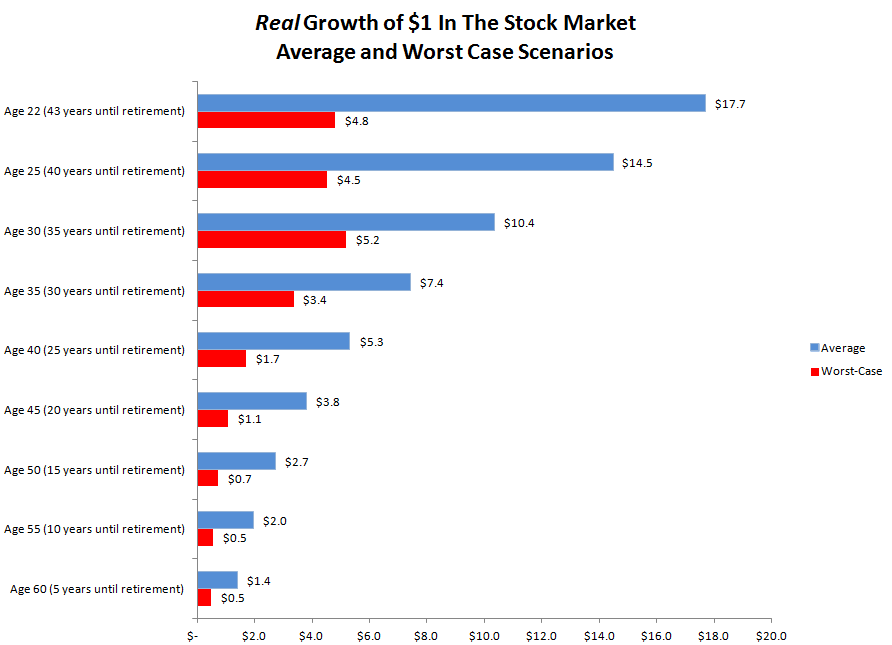

Obviously we want every dollar we invest to be worth as much as possible when we retire. The first figure below lists the average result for $1 invested in the stock market at various ages. It shows what each dollar will be worth by age 65 depending on when you start investing in the stock market (earlier if obviously much better). This assumes the market grows at the same real rate it has since 1926 (6.9% per year). “Real” means after accounting for inflation, which reduces your returns. For the reasons I lay out in a separate piece on the history of money, inflation is a crucial consideration when evaluating investment options.

One important note: I am basing this analysis on data back to the 1920’s for stocks, bonds, and cash (bills) because it allows us to include events as diverse as the Great Depression, World War II, runaway inflation, booms, busts, panics, and so on. Everything short of a 100% breakdown is covered.

Note that the earlier you start, the more potent each dollar is. If you start at 22, then each dollar would be worth nearly $18 when you retire…but if you procrastinate, even until you are 40, each dollar would only be worth $5.30.

Millennials care more about risk than anything else, so let’s look at the worst case scenario alongside the average. These numbers represent the worst possible times to be invested (again starting at various different ages) between 1926 and 2014.

Sure enough, stocks are risky as hell in the short-term. Look at the worst-case scenario for the value of a dollar invested by people 50 years or older (who have between 5-15 years until retirement). It would be terrible to invest in the stock market at age 50 and have each dollar worth just 70 cents 15 years later. That’s a scary 30% decline over 15 years.

But look at the worst case scenarios if you start younger. If you start at age 22, the worst result for a dollar invested was growth to $4.80. This would have happened if you invested at age 22 in 1966 and retired in February 2009 at the exact market bottom of the second worse collapse in the stock market’s history. It also would have included the crash in 2000 and the miserable period for stocks between 1968 and 1982 when the market went nowhere. Even through three tumultuous markets, you’d still have $4.80 for every dollar you invested.

You can see why risk cannot be assessed independent of time. Stocks can be very risky in the short term, but have been extremely safe over the long term, which is all that should matter to millennial investors.

Bonds and Cash

What about the “safe” options that millennials prefer? Here are the average and worst case scenarios for bonds and cash (t-bills).

For both bonds and bills, the worst case scenarios are scary across all time periods. Even if you start investing when you are in your 20s, there is a chance that each dollar you put into bonds or bills will be worth less than 50 cents in real terms come retirement. For bonds and bills, inflation is the silent killer. Bonds and cash (bills) seem so safe because they preserve the number of dollars you have. But what good is preserving $100 until 2050 if a sandwich costs $80 at that point in the future? Purchased power is what matters, not the number of dollars you have. Judged this way, stocks are the runaway winner.

Think back to the current millennial investor’s allocation. More than 50% is in cash, an asset that seems safe, but can be very dangerous over the long-term. Meanwhile, millennials have just 28% in stocks, which even under the worst-case scenario have delivered strong long-term real returns.

What If The Sky Isn’t Falling?

I’ve focused on worst-case scenario because millennials are so sensitive to risk…but the best case scenarios are also worth considering. Here is the best case scenario for each dollar invested at different ages for all three assets: stocks, bonds, and cash.

If you start investing in the stock market in your 20s, there is a chance each dollar ends up being worth much more than the $4.80-worst-case scenario or $18-average. There was one period where each dollar grew to $52 over 40 years. In sharp contrast, the best case over 40 years for bonds and bills was $6.70 and $1.90, respectively.

When Safe Isn’t Safe

Millennials are right to be cautious, but if their current investment allocations are any indication, too many millennials are thinking about short-term risk when they should be thinking about very long-term risk. When risk is reframed, stocks have always been the safest long term asset. The bottom line is that you should start investing now. Even if the initial amounts are very small, the long-term benefits are can be huge. But you have to start young and remember that what seems risky is in fact safe.

Monthly real returns for stocks, bonds and bills from Roger Ibbotson. Stocks = S&P 500, Bonds = Long Term U.S. Government Bonds, Bills = T-Bills